Indian companies and individuals owed Rs 4.1 lakh crore to public sector banks in overdue loans in the “non-priority sector”–mainly corporate lending, car loans, personal finance, credit card dues and home loans–as of March 2016. These non-performing assets (NPAs), if fully recovered, would suffice to pay off distressed farm loans across eight states, with a-third (32%) still left over, an IndiaSpend analysis of Reserve Bank of India (RBI) data shows.

In the decade to 2016, non-priority sector bad loans rose more than 22-fold (2166%) from when they were valued at Rs 18,300 crore in 2006. During the same period, the sector’s share in public sector banks’ NPAs rose from 44.2% to 76.7%. This growth was particularly pronounced after 2011–12-fold (1110%) in five years.

Public sector banks’ bad loans in the priority sector–which includes loans for agriculture, micro and small enterprises (MSMEs), small-scale industries, education, affordable housing and renewable energy–also grew during the same period, but slower. These grew five times (465.8%) from Rs 22,200 crore in 2006 to Rs 1.25 lakh crore in 2016, although their share in the total NPAs of public sector banks shrank by more than 55% (thanks to the growth of non-priority sector NPAs).

Source: Reserve Bank of India

Agriculture-related bad loans, valued at Rs 48,467 crore, comprise the third largest NPAs, after corporate NPAs (Rs 3.16 lakh crore) and MSME NPAs (Rs 74,051 crore), according to this 2016 Lok Sabha reply.

“For non-priority loans, NPAs result when business models go wrong. They are normally linked to sectors rather than individuals–which is the case of farm loans, where the monsoon plays an important role,” Madan Sabnavis, chief economist of Credit Analysis & Research Ltd, a ratings agency, told IndiaSpend. “An economic downturn increases chances of NPAs as companies cannot service their debt. When there is no malafide intent or managerial incompetence, it is mainly such external conditions that lead to corporate NPAs. For farm loans it is more straight-forward and linked to monsoon,” Sabnavis said.

RBI officials refused to comment for this story.

85% jump in write-offs as NPAs eat into banks’ lending capacity

Source: Reserve Bank of India

As of March 2016, 7.5% of all lending in India–by public, private and foreign banks, to both priority and non-priority sectors–amounting to Rs 6.1 lakh crore had become non-performing assets. This is more than twice the union budget for defense at Rs 2.6 lakh crore in 2017-18, which received the highest allocation among all central ministries this year.

This is the highest recorded gross NPA ratio in the last 10 years, RBI data show. Prior to 2014, the ratio typically remained below 4%.

Such high NPA ratios limit banks’ ability to lend money to productive sectors.

An asset quality review introduced in April 2015, through which the RBI forced banks to finally recognize their stressed assets as NPAs and record them as such on their balance sheets, was the key reason why NPA ratios apparently rose from 2014-15 onwards.

The review unearthed numerous cases of loan “restructuring”–giving the borrower some concessions to avoid a default–and dressing up of account books. Over a decade, NPA write-offs jumped 85% from Rs 8,799 crore in 2006 to Rs 59,547 crore in 2016, according to this 2016 Lok Sabha reply.

The trend is significant, a former senior RBI official told IndiaSpend. “All provisions against write-offs eat into the capital of the bank, reducing its capacity to lend. The sharp slowdown in credit growth over the past couple of years is significantly attributable to banks’ unwillingness to take on any further risk of write-offs, which would reduce their capital even further,” the official wrote in an email, requesting not to be named. From a policy perspective, he explained, to sustain nominal GDP growth of 12-13 per cent, credit should grow at least at that rate, if not faster. (Nominal GDP is estimated at current prices, not taking inflation into account, while real GDP is estimated at constant prices after accounting for inflation.)

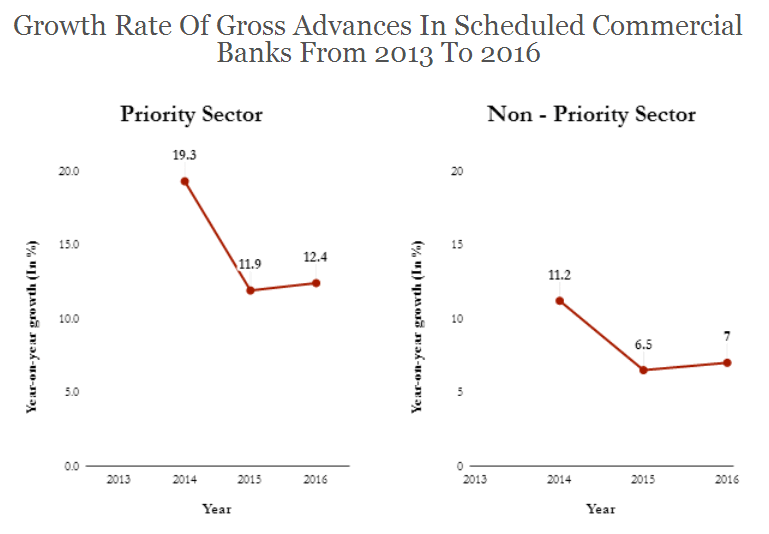

This is evident from the waning stream of credit advances to both priority and non-priority sectors in recent years. While the volume of credit has risen in absolute terms, its year-on-year growth has slowed, RBI data show. Growth of lending in both sectors slowed by more than 35% — from 19.3% in 2013 to 12.4% in 2016 in the priority sector, and 11.2% in 2013 to 7% in 2016 in the non-priority sector.

Source: Reserve Bank of India

“If [bank] capital is being eroded by loan losses, infusions are needed, either from the government or from the market. Neither is looking feasible at the moment. So, sooner or later, slow credit growth will impede GDP growth,” the former RBI official said.

Commercial banks’ aggressive long-term lending caused the NPA problem

Most of the experts IndiaSpend spoke to for this story agreed that much of the NPA problem arose when commercial banks lent aggressively, for long durations, to the non-priority sector in the early 2000s, when the economy reached a growth rate of over 9% in 2005-06, 2006-07 and 2007-08.

“About half the NPAs in the system are in the infrastructure sectors. A substantial portion of the remaining are in sectors such as steel, which have been subject to various business shocks. These are mostly loans for capital expenditure and are long term,” the former RBI official told IndiaSpend. “Priority sector loans, on the other hand–crop loans, for example–are more often short-term loans for working capital purposes,” he explained.

The global economic slowdown of 2008 ushered in a prolonged period of uncertainty in India as elsewhere. Exports fell, some mining projects faced regulatory bans, sectors such as power and iron and steel faced difficulty getting permits, raw material prices fluctuated and infrastructure projects faced power shortages. All these factors, coming on top of aggressive past lending by banks, caused NPAs to swell, Finance Minister Arun Jaitley told the Lok Sabha in 2016.

During the early 2000s, when banking reforms were gathering pace, development finance institutions (DFIs) such as IDBI, ICICI and IFCI began to lose ground. DFIs had been created to provide medium- to long-term credit for industrial projects, and supplement commercial banks’ offering of short-term credit for working capital.

Initially, the government made low-cost capital available for DFIs, but withdrew subsidized funding in the early 1990s, leaving DFIs to rely on capital markets to raise funds. Further, a significant chunk of their loans to projects in the steel, textiles and basic chemicals sectors, among others, began to experience delays and cost escalations, turning loans into NPAs, as this Hindu Business Line report from January 2002 explains.

When DFIs consequently hiked their lending rates, they became uncompetitive against commercial banks that were now rapidly increasing their long-term portfolios as post-liberalization reforms had opened up the banking sector to private and foreign players.

“Since 2002 commercial banks started lending more long-term loans compared to earlier when the bulk of their lending was short-term–working capital and trade credits,” Pronab Sen, country director for the India programme of the International Growth Centre, a New Delhi-based think-tank, told IndiaSpend. “In 2002, short-term credit accounted for 73% of bank loans–this is down to 45% now.”

As of March 2016, medium- and long-term loans had touched almost 50% of total loan portfolio, according to this Hindu Business Line report from April 2017.

Share of corporate bad loans rose 67% after 2010-11

The share of non-priority NPAs in public banks rose from less than half in 2011 (45.9%) to greater than 3/4th (76.7%) of total NPAs in 2016. Meanwhile, the share of priority sector NPAs shrank by more than 55% (thanks to the growth of non-priority sector NPAs) from 53.8% in 2011 to 23.3% in 2016.

Source: Reserve Bank of India

Infrastructure lending is also implicated as a major culprit in this Economic & Political Weekly (EPW) report from March 2017, which says banks tried to push these loans in an attempt to stymie the effects of the 2008 global economic crisis.

As the regulator, the RBI relaxed income-recognition norms and allowed banks to restructure firms’ loans instead of allowing these to turn into NPAs. “This made it easier for already over-leveraged [or financially over-burdened] companies to borrow more,” the EPW report said. Between 2010 and 2012, the borrowing capacity of these companies further grew while their underlying financial situation worsened. By 2011, the Indian economy officially entered into a recession as demand started to slow down.

“From the dramatic growth years of the 2003-08 period, real GDP growth rate during 2011-13 slowed down to 6%. New projects failed to take off due to the lack of government approvals and projects that had received credit during the credit boom period got stalled owing to the general slowing down of the economy. The problem was especially acute in the infrastructure sector. This led to a fresh wave of NPAs, especially in sectors such as infrastructure, steel, metals, textiles, etc,” the EPW report said.

In 2016, fraud NPAs accounted for 7.15% of all NPAs

Commercial banks had enhanced lending for long-gestation projects even as they had little expertise or experience in assessing such projects’ creditworthiness.

As a result, data showed that 7.15% of total gross NPAs as on March 2016 constituted fraud, as Finance Minister Arun Jaitley admitted in a reply to the Lok Sabha in 2016.

“This is even an greater worry [than the growth of NPAs or write-offs] because it directly reflects that risk assessment is not strong and it’s not the external environment but lacunae in the systems that has led to this,” Sabnavis of the credit rating agency said.

Since 2013, recovery of bad loans has dropped 53%

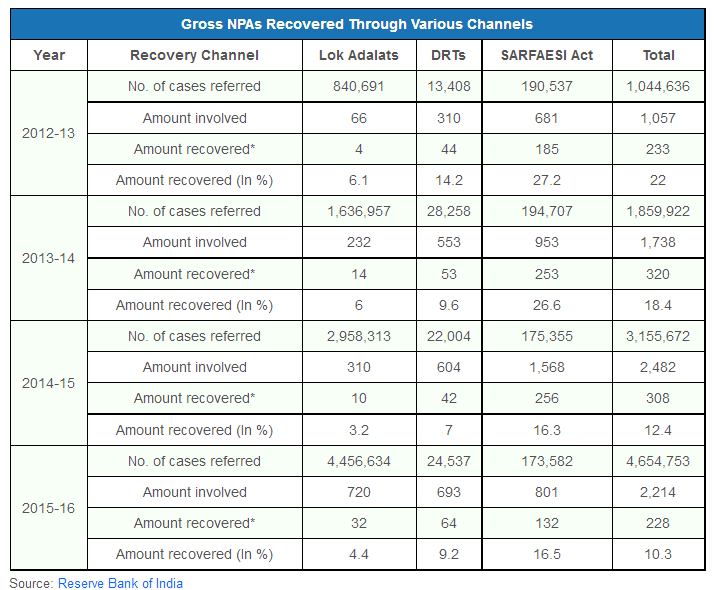

While NPAs and write-offs have leaped ahead unchecked, bad loan recovery has failed to keep pace. Since 2013, NPA recoveries have halved from 22% in 2013 to 10.3% in 2016, RBI data show. Recovery dropped from 18.4% in 2014 to 12.4% in 2016.

The government has advised banks to act against guarantors of defaulting borrowers under relevant sections of the Securitization and Reconstruction of Financial Assets and Enforcement of Security Interest (SARFAESI) Act, 2002, and other laws such as the Indian Contract Act, 1872,and Recovery of Debts due to Banks and Financial Institutions Act, 1993, etc., Jaitley said in his 2016 Lok Sabha response.

Of the 4.6 million cases referred to various recovery channels, RBI data show, 95.7% were referred to the alternative dispute resolution forums of Lok Adalats; 3.7% for prosecution under the SARFAESI Act, 2002, which allows banks and other financial institutions to auction properties to recover loans; and 0.5% to Debt Recovery Tribunals (DRTs), which work expressly to recover banks’ and other financial institutions’ debts.

While the number of cases referred to these channels has risen over four-fold since 2013, actual recovery has dropped by nearly half (44%) since 2015, data show.

Bad loan recovery under the SARFAESI Act–which accounted for the most money recovered–witnessed the biggest decline, of 40% between 2015 and 2016. Though loan recovery through Lok Adalats and DRTs picked up in 2016, the loans recovered in 2016 are still lower in value than the recovery in 2013.

In 2015-16, banks recovered Rs 22,800 crore of NPAs, lower than the amount recovered in 2013-14 (Rs 23,300), RBI data show.

Corporate NPAs v. farm loans waivers

Besides recovering NPAs through these channels, Jaitley also said the government and the RBI have undertaken measures such as setting up a joint lenders’ forum, a strategic debt restructuring scheme and a scheme for strategic structuring of stressed assets to resolve bad loans.

However, these measures appear to undo the work of the RBI’s asset quality review undertaken in 2015. Debt restructuring merely helps banks brush NPAs under the carpet, experts told IndiaSpend.

“Treating them [non-priority NPAs] as restructured assets where you increase the repayment periods and lower the interest rates delayed the inevitable. They should’ve been recognized earlier itself,” said Sabnavis. “‘This evergreening’ of stressed assets–giving a new loan to pay off the earlier loan–is common practice. The RBI is trying to prevent this from happening,” Sen from the India programme of the International Growth Centre told IndiaSpend.

Although the government appears eager to give non-priority sector corporate borrowers some leeway in repayment, it is quite likely to give into loan waiver demands, as IndiaSpend reported on June 15, 2017.

While corporates have assets to use as collateral for more borrowings, farmers–85% of whom are small and marginal–are too poor to qualify for more loans. Further, experts reason, the central government bears the responsibility for NPA resolution and state governments for loan waivers.

“Farm loans do have special features such as a six-month servicing period compared to three months for other sectors and in the case of natural disasters the loans are rolled over for a period of upto three years,” Sen told IndiaSpend.

But these are not blanket provisions, he explains in this report published in Mint on June 23, 2017. The measures are only applicable to farmers of officially designated ‘affected districts.’ The provision was already invoked in 2014 and 2015 in Maharashtra when the region witnessed drought, alleviating distress somewhat.

“The year 2016-17 is different. There was no drought or any other natural calamity. The farmers’ problems are almost entirely the outcome of demonetization… practically all farmers have suffered, and there has been no rolling over of their loans. As a consequence, farmers across the country have to either agitate or face the prospect of default,” Sen wrote. “While waivers absolve the farmer of all liability, defaults entail serious consequences such as loss of collateral, if any, and loss of access to future bank loans.”

Last week, after reporting a spike in its own NPAs “due to farm loan waivers,” HDFC Bank warned that lenders may discontinue fresh loans to the agriculture sector, The Economic Times reported on July 28, 2017.

“Banks are likely to see increase in NPAs in the agriculture sector and a general worsening of credit culture… Loan waivers are likely to also impact the supply of credit as fresh lending to the agriculture sector could dry up,” the bank’s economists said in a note.

To be sure, waivers come with the imminent possibility of ‘errors of inclusion’–even those farmers who do not need a waiver get it–making it an expensive prospect for the state exchequer, as the HDFC economists pointed out in their note.

However, defaulting on farm loans exposes the sector that employs 56% of India’s workforce to a heavy penalty. It may force the most distressed and the most vulnerable out of access to formal credit and possibly out of farming as well, Sen told IndiaSpend.

So should lenders waive farm loans? Or should they “restructure” non-priority sector NPAs? “The main consideration here is [that] a lot of the non-priority NPAs are large and valued customers of the banks, who also have considerable political clout,” Sen told IndiaSpend.

Non-performing asset or bad loan: An asset, including a leased asset, that ceases to generate income for the lender

Restructuring: When a lender grants concessions to the borrower to avoid a default. Restructuring can involve alteration of repayment period or amount, change of the amount or number of installments, and lowering of the rate of interest.

(Saldanha is an assistant editor with IndiaSpend.)

Courtesy: India Spend